How to Set Up Budget Categories That Actually Work

Most budgeting apps come with preset categories — Housing, Food, Transport, Entertainment. These generic labels feel intuitive but often fail in practice because they don't reflect how you actually think about your money. When every grocery store purchase, restaurant meal, coffee shop visit, and snack run gets lumped into a single 'Food' bucket, you lose the granularity needed to make meaningful spending decisions. You might discover you spent $600 on 'Food' this month, but without knowing how much was groceries versus dining out versus impulse snacks, that number tells you very little about where to cut back.

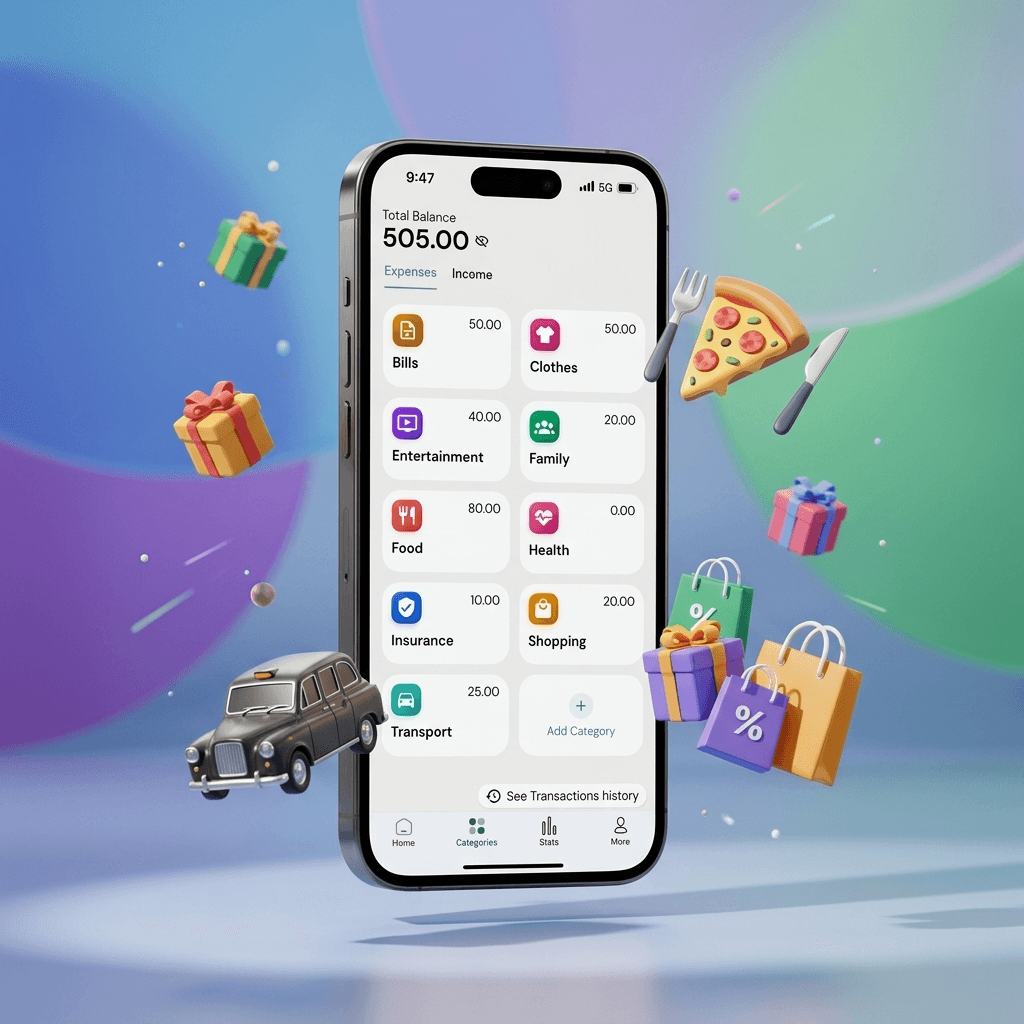

In Easymony, every category is custom

You create them from scratch, name them exactly as you like, and color-code them for instant visual recognition. This flexibility is powerful, but it requires some upfront thinking. The good news is that setting up categories well takes about 15 minutes, and once done, it makes every subsequent transaction entry faster and more meaningful. Think of it as investing a small amount of time now to save hours of financial confusion later.

Start by listing every regular expense in your life — not by category, but as raw items

Rent, electricity, Netflix, gym, groceries, eating out, petrol, insurance, phone bill, streaming services, hobbies, clothing, medical expenses, pet supplies, and so on. Don't worry about organizing them yet — just dump everything onto a list. Include irregular expenses too: annual subscriptions, holiday gifts, car maintenance, medical checkups. The goal is to capture the full spectrum of your financial life before you start grouping things.

Once you have this list, group them into clusters that make logical sense to you

This is where personalization matters. One person might group all transportation costs — petrol, bus fare, Uber rides, car insurance — into a single 'Transport' category. Another person might want to separate 'Commute' from 'Travel' from 'Car Maintenance.' Neither approach is wrong. The right categories are the ones that match how you think about your money, not how an app developer guessed you might think about it.

For most people, 8-12 categories is the sweet spot

Too few and transactions get lost in broad buckets; too many and entering transactions becomes tedious. Aim for categories that are distinct enough that you never wonder which one to use. If you find yourself hesitating between two categories when logging a transaction, those categories probably overlap too much and should be merged or clarified. The best category system is one where every expense has an obvious home.

This is where Easymony's subcategory feature becomes a game-changer

Subcategories let you organize each budget category into more specific groups without cluttering your main category list. For example, your main 'Insurance' category can have Health, Car, Home, Life, Travel, Device, Business, Pet, Premiums, Claims, Renters, and Disability subcategories. You get granular tracking without a bloated category list. The two-level structure — Category → Subcategory — gives you the best of both worlds: simplicity at the top level and detail when you need it.

Here's a practical category framework that works well for most individuals: Housing (rent/mortgage, utilities, maintenance), Food (groceries, dining out, snacks), Transport (commute, fuel, insurance), Personal (healthcare, clothing, grooming), Entertainment (streaming, hobbies, events), Savings (emergency fund, investments, goals), Debt (credit cards, loans, student debt), and Miscellaneous (gifts, donations, unexpected expenses)

Start with this framework and customize it based on your actual spending patterns.

For freelancers and small business owners, your category system should separate personal and business expenses from the start

Create parallel category sets — one for personal spending and one for business. Easymony's multiple accounts feature makes this even easier: create a 'Personal' account and a 'Business' account, each with their own category structure. This separation will save you enormous headaches at tax time and give you a clear picture of your business profitability.

Color-coding your categories is more important than it sounds

Easymony lets you assign a unique color to each category, and this visual distinction helps you process your spending at a glance. When you look at a pie chart of your monthly expenses, you should be able to instantly identify which slice is which without reading labels. Choose colors that feel intuitive — green for savings, red for debt, blue for housing, orange for food. Over time, these color associations become automatic, making your financial dashboard even faster to read.

Revisit your categories after 30 days of use

You'll quickly discover which ones you use frequently and which ones you never touch. Don't hesitate to rename, merge, or split categories — Easymony makes this seamless. Your category system should evolve as your life changes. A new baby, a move to a different city, a career change — all of these life events will shift your spending patterns, and your categories should shift with them. The beauty of a custom category system is that it grows with you.

One common mistake is creating categories based on how you want to spend rather than how you actually spend

It's tempting to set up a 'Savings' category with an ambitious monthly target and then feel guilty when you consistently miss it. Instead, start by tracking your actual spending honestly for a month or two, then set category budgets based on real data. Once you understand your baseline, you can gradually adjust categories to align with your financial goals. Realistic categories that reflect your actual behavior are far more useful than aspirational ones that make you feel like a failure.

The best budget categories are the ones you'll actually use consistently

Keep them simple, make them personal, and don't be afraid to change them as your financial life evolves. Easymony gives you the tools to build a category system that works for your unique situation — use them.

Related Articles

Why Offline-First Apps Are the Future of Personal Finance

We explain our technical decision to use an offline-first database. Learn how skipping cloud sync not only makes the app lightning fast but also ensures your financial data never leaves your device.

Mastering PDF Reports for Better Budgeting

Generating a transaction history PDF is just the beginning. Discover how to use Easymony's reporting tools to analyze your spending trends and cut unnecessary expenses at the end of each month.